4 November 2021

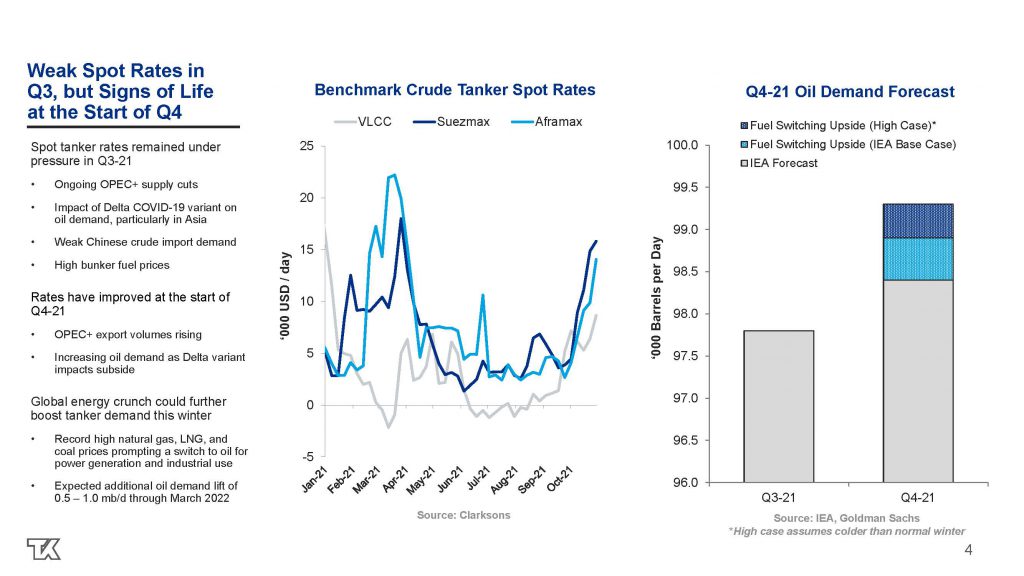

Crude tanker spot rates fell to multi-decade lows in the third quarter of 2021. The primary reason was a continued lack of crude oil trade volumes as ongoing OPEC+ production cuts and various non-OPEC+ supply outages, coupled with a continued drawdown of oil inventories due to a backwardated oil price structure, weighed on crude tanker demand. Crude tanker spot rates were also impacted by the Delta COVID-19 variant during the quarter, which led to reduced mobility and lower oil demand in several regions, most notably in Asia. Asian crude oil imports were further impacted by weaker oil demand in China, as the country cut import quotas for independent refiners. Lastly, higher bunker fuel prices, which rose in tandem with crude oil prices, also weighed on crude tanker spot rates during the third quarter.

Crude tanker spot rates have shown modest improvement at the beginning of the fourth quarter of 2021 as global crude oil trade volumes have begun to recover. The OPEC+ group has been increasing crude oil supply at a rate of 0.4 million barrels per day (mb/d) per month since August 2021, and this has led to an increase in exports out of key load regions such as the Middle East and West Africa; however, as of October 2021, the OPEC+ group still had an estimated 4.6 mb/d of supply cuts in place. The unwinding of OPEC+ cuts is expected to continue in the coming

months which, coupled with rising non-OPEC+ production, should result in an increase in global oil production of 2.7 mb/d between September 2021 and the end of 2021 according to the International Energy Agency (IEA). Global oil demand is expected to increase over the winter, boosted by the ongoing energy supply crisis and record high prices of coal and natural gas, which has encouraged switching to oil for power generation. According to the IEA, oil demand could increase by more than 0.5 mb/d compared with normal winter conditions due to gas-to-oil switching,

particularly if the northern hemisphere experiences a cold winter. The above factors, coupled with normal winter market seasonality, could lead to an improvement in crude spot tanker rates through the rest of the fourth quarter of 2021 and into early 2022.

Looking further ahead, the recovery in global oil demand is expected to continue in 2022 as increasing vaccination rates are anticipated to result in a higher level of global mobility. The IEA forecasts an increase in global oil demand of 3.3 mb/d in 2022, lifting oil demand above pre-COVID levels. However, some forecasters are more optimistic, with OPEC projecting an increase of 4.2 mb/d next year. With global oil inventories currently well below the 5-year average, more oil supply will be needed in order to meet growing demand. The OPEC+ group announced plans to continue unwinding its supply cuts at a rate of 0.4 mb/d per month next year until cuts are fully unwound by September 2022. In addition, non-OPEC+ supply is expected to increase by just under 2 mb/d next year. This includes higher production from the United States, Brazil, and Guyana, which are key load regions for mid-size tankers. Crude tanker demand is therefore expected to improve during 2022.

The outlook for tanker fleet supply continues to look positive. New tanker ordering ground to a virtual halt in the third quarter of 2021 with just 0.75 million deadweight tons (mdwt) of new orders placed, which is the lowest quarterly total since the second quarter of 2009. Elevated newbuilding prices, which are currently the highest since 2009, are expected to limit newbuild orders in the near-term. The third quarter of 2021 also saw an increase in tanker scrapping with 4.7 mdwt removed, the highest quarterly scrapping total since the second quarter of 2018. A combination of low tanker ordering and higher scrapping bodes well for limiting the level of future fleet growth. The Company currently estimates approximately 2 percent tanker fleet growth in both 2021 and 2022, and minimal fleet growth in 2023, as scrapping is expected to largely offset new vessel deliveries.

In summary, the tanker market has seen a period of exceptionally low spot rates in 2021 to-date. However, the tanker market is experiencing an improvement at the start of the fourth quarter and increasing trade volumes, coupled with a potential oil demand boost due to the global energy crunch and seasonal weather delays, could support rates further over the winter months. Looking further ahead, tanker supply and demand fundamentals continue to trend in a positive direction, which should lead to higher tanker fleet utilization and improved tanker rates in the future.