12 May 2022

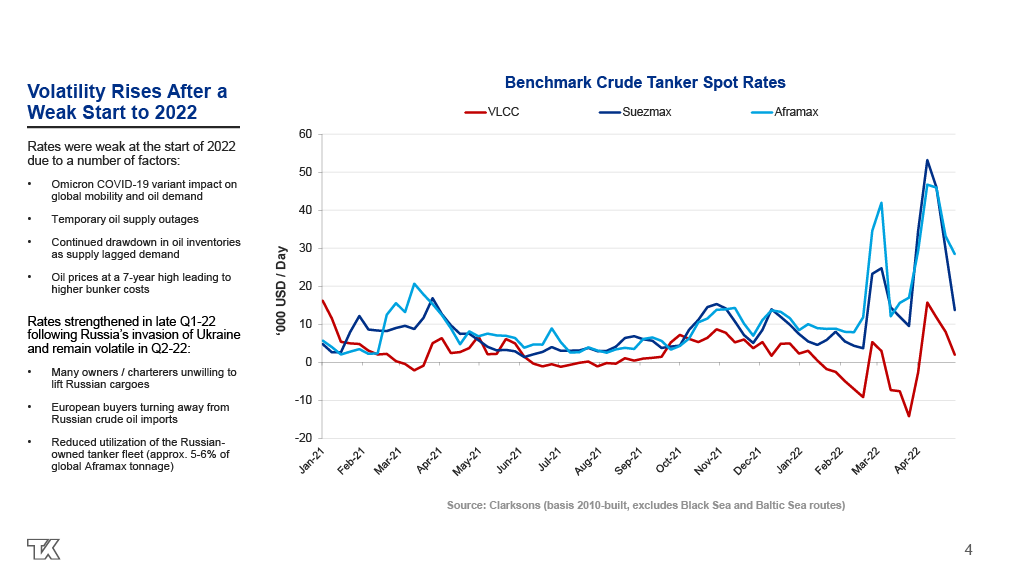

Crude tanker spot rates were relatively weak during the first two months of 2022 due to the impact of the Omicron COVID-19 variant on oil demand, lower than expected oil supply growth due to temporary production outages, and high crude oil prices which led to an increase in bunker costs. However, Russia’s invasion of Ukraine in late February led to a spike in crude tanker rates, particularly in the Aframax and Suezmax sectors, due to trade disruptions and the rerouting of cargos. Since then, the tanker market has exhibited significant rate volatility and stronger crude tanker spot rates.

Although the near-term outlook for the tanker market is uncertain, changing trade patterns due to the Russia-Ukraine conflict are resulting in an increase in tanker tonne-mile demand. During the past few weeks, there has been a decrease in Russian crude oil exports to Europe and a corresponding increase in Russian crude oil exports to Asia, particularly to India. This has been positive for tanker tonne-mile demand due to longer voyage distances. Similarly, Europe is having to replace Russian crude oil with imports from further afield, including the U.S. Gulf, West Africa, and the Middle East, which is also positive for tanker tonne-mile demand. Given the European Union’s recent proposal to phase out all Russian crude oil imports over the next six months, and refined products by the end of 2022, the Company expects that these altered trade patterns may persist for an extended period of time. In addition, the fleet of Russian-owned and operated ships, which comprises approximately 5 percent of the global Aframax fleet, is finding it more difficult to trade, which is further tightening available fleet supply.

The outlook for the global economy and oil demand has worsened since the start of the year due to rising inflation, Russia’s invasion of Ukraine, and a resurgence of COVID-19 cases, particularly in China. In its April 2022 “World Economic Outlook” report, the International Monetary Fund (IMF) reduced its GDP growth outlook from 4.4 percent to 3.6 percent and warned that risks are weighted to the downside. In addition, the International Energy Agency (IEA) has downgraded its outlook for global oil demand growth from 3.2 million barrels per day (mb/d) at the start of the year to 1.9 mb/d in its April 2022 report. A weakened outlook for the global economy and oil demand is a potential headwind for tanker rates in the coming months; however, these negative impacts may be offset by the increase in average voyage distances due to the Russia-Ukraine conflict and the Company expects rate volatility to persist in the near-term.

The outlook for tanker fleet supply continues to look very positive, with some of the best supply fundamentals seen in over two decades. As of April 2022, the tanker orderbook stood at only 6.4 percent of the existing fleet size, which is the lowest since Clarksons started tracking orderbook data in 1996. Rising newbuilding prices, which are currently the highest since 2009, and a lack of shipyard capacity continue to limit new tanker orders, with just 0.2 million deadweight (mdwt) of new orders placed in the first quarter of 2022, the lowest since at least 1996. With most major shipyards being at capacity through the middle of 2025, there is limited available capacity to order new tankers for delivery in the next three years. This, coupled with a rapidly aging global tanker fleet, should lay the foundation for very low fleet growth in the medium-term.

In summary, spot tanker rates have increased following Russia’s invasion of Ukraine and look to remain volatile in the coming weeks and months as the situation continues to unfold. Although the near-term outlook is highly uncertain, the longer-term outlook appears positive due to a small tanker orderbook, very low levels of tanker ordering, and an aging global tanker fleet, which together should lead to an extended period of very low tanker fleet growth.